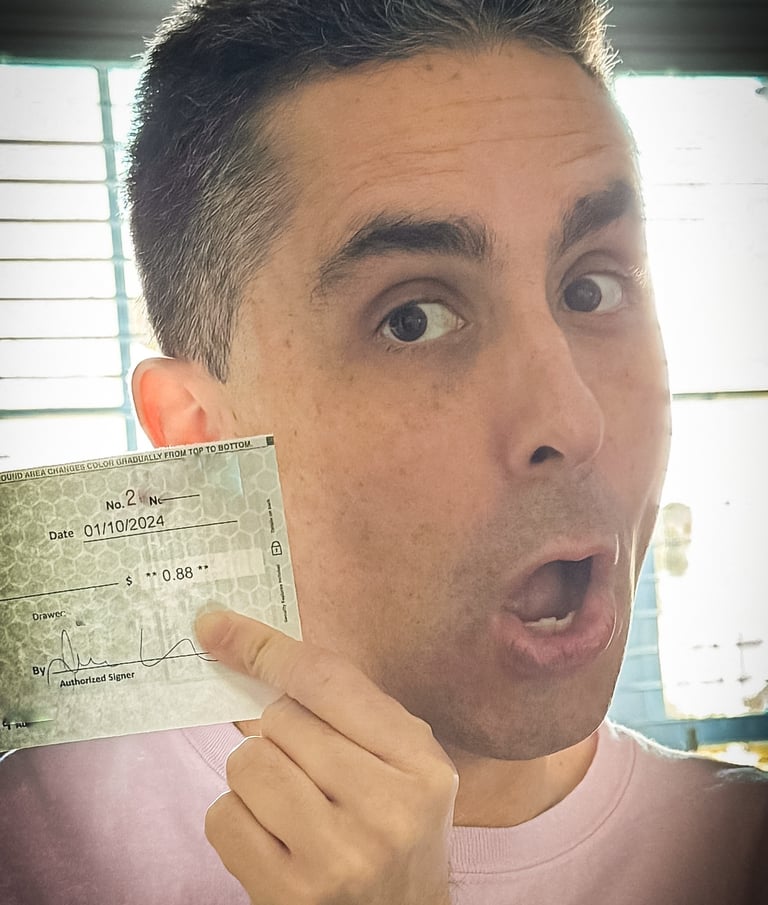

Did I shave my face for this? 👨🏫 A lot of hassle for 88 cents, but operational mishaps go much deeper than that.

As I often advocate for, as a banking customer, you need to be proactive in finding the banks that offer you the best services and especially the highest interest rates on your money while we are in a higher interest rate environment. As a result, I opened a new account with a bank I had not used before in November 2022. They were offering the highest interest rate amongst the local banks on a money market account, so I decided to give them a shot since most of my money is with non branch or digital experience banks that pay more interest, but lack a local touchpoint. It started off well, but deteriorated fairly quickly as bank operations couldn't keep up with the changing rate environment and support people were not empowered to manage the business. Here’s a quick summary of where things broke down for this bank from my perspective as a previous bank operations manager for 20 years.

Jason Herman

1/30/20245 min read

As I often advocate for, as a banking customer, you need to be proactive in finding the banks that offer you the best services and especially the highest interest rates on your money while we are in a higher interest rate environment. As a result, I opened a new account with a bank I had not used before in November 2022. They were offering the highest interest rate amongst the local banks on a money market account, so I decided to give them a shot since most of my money is with non branch or digital experience banks that pay more interest.

Here’s a quick summary of where things broke down for this bank and the facts behind them from my perspective as a previous bank operations manager for 20 years:

1. Branch management personnel failed to respond to easy email questions sent to them on multiple occasions.

2. Being hustled to deposit more money in order to get the higher interest rate you are advertising to new customers and that is more in line with risen rates and competitor’s offerings seems outside of the norm in today’s compliance risk climate. Consider giving an existing customer the same rate. You can’t afford to play rate games with strong online competitor offerings and risk customers leaving.

3. Empower your outsourced customer service professionals. They are nice and polite, but can’t resolve any real issues without involving the branch or onshore bank team members.

4. Figure out why it takes a customer having to go to these lengths to close an account they wanted closed months ago. There’s a breakdown operationally. If you can’t resolve something this simple, what else is broken and why would I trust you with my money?

My experience with the bank was generally positive. People were friendly and they were well staffed. About 6 months after the account was opened, I noticed they were offering about 1% more for new customers than they were paying for my same money market account. The old cell phone play of offering better deals to win new business and not permitting existing customers to benefit. I get this from a business standpoint, but as the cell phone companies and others have learned, that usually backfires on you with customers switching their service.

I tried to reach out to my local branch about how I could get the new rate, but they must have been too busy to respond to my emails. I then reached out to their national call center, which I would come to learn was staffed mostly by an outsourced, off shore team. Very nice and polite, but could not help. They passed me back to an on shore group to handle what would be a “negotiation” to get me to the new, higher interest rate. Basically, give us substantially more “new” money if you want the new rate and that was the best they could offer. I did think a little bit about what their fair and responsible banking group must have thought about this sales approach. Not sure we would have won that battle at similar companies I have worked.

Needless to say, the bulk of my money left that bank the next day via ACH for a digital bank that paid even more. I kept a little in there for local convenience for another 6 months, but then decided to close the account since it was no longer needed. I went into the branch to get things closed, and everyone was super helpful. However, I was a bit surprised no one ever asked me why I was closing an account that had once been well funded. I took my cashier’s check and moved on, nonetheless. The next bank was happy to have the deposit.

Well, that is until a few days later when I started getting low balance alerts that I had 88 cents still in the account (the branch or system had not calculated the final interest payment correctly). I reached out to the branch, but could not get a response. Then I tried the outsourced call center, which was fast to give me the same textbook answers every time I called. Having managed call centers myself, I quickly recognized they wanted to get me off the phone and that the answers reflected a lack of concern or more likely, the ability to fix the issue. They assured me eventually that it would reconcile at month end and I’d be sent that lucrative 88 cents and the account properly closed.

Fast forward a couple months.. Guess what was still there? Of course, 88 cents sitting in the account. Well below the minimum balance of the account and my account was prime for becoming a delinquent account with bank fees for that reason. These type of situations happened at the bank I worked at also and were also a source of great customer and back office operational pain when they were finally discovered. You can’t just let a concern sit and hope that it self rectifies itself.

I figured it had been long enough and after a few more frustrating attempts to get the account properly closed, I knew it was time to reach out to the CEO of the bank. Ironically, the outsourced call center team, had no idea who that even was. I wrote a polite note to the CEO and waited for someone in his executive communications group to contact me. That is usually who responds to 99% of those emails and they have the ability to get things corrected when other groups can only read from a script or push you off to someone else.

As expected, I was contacted 24 hours later by a gentleman who knew how to fix this issue. He had the local branch send me a check for that pesky 88 cents. Overnight mail, by the way. I always cringe when I hear stories about having to spend $20 in postage to resolve something that was a simple fix for much less money. As I always told them, this was not about the money (I offered them to donate it to whatever charity they chose), but more about closing the account and avoiding negative balances.

At the end of the day, this was a first world problem for sure. However, it demonstrates a break down in one institutions abilities to properly address the needs o its customers and reveals some weakness in back end communication and processing. I always say customers are funny about their money and if they can’t trust you to properly handle small things like I was requesting, why would they want to keep their money in your bank or utilize you for other services? Having the right teams and them trained and empowered to assist customers is critical to first retaining existing customers (and your hard working teammates) and then to grow the business further by taking from those who have not taken a hard look at cracks in their processes and procedures, as well as service levels.

#bankoperations #customerloyalty #Fairandresponsiblebanking #evaluateyourprocesses